Consolidated or categorised expenses? What Making Tax Digital IT really requires

HMRC’s Making Tax Digital for Income Tax (MTD IT) changes not only how businesses keep records, but also how expenses can be reported to HMRC in the required quarterly updates. These updates are a year-to-date summary of income and expenses from self-employment and/or property income.

When it comes to reporting expenses, there is often confusion is the difference between consolidated and categorised expenses.

The good news is that many self-employed individuals or those with property income do not need to submit detailed expense breakdowns every quarter at all.

Understanding the difference can help businesses choose an approach that feels proportionate and manageable while still staying compliant with HMRC requirements.

What are consolidated expenses?

Consolidated expenses are sometimes referred to as “three-line accounts”. Instead of reporting detailed expense categories, for MTD IT a business simply submits:

- total income

- total expenses

For many smaller businesses and those with property income, this can make quarterly reporting significantly simpler. Rather than allocating every expense to a detailed category before submission, businesses can maintain a simpler reporting process while still meeting MTD IT obligations.

This flexibility is particularly helpful for individuals who:

- manage relatively simple finances

- prefer working with spreadsheets

- do not use full bookkeeping software

- want to minimise administrative burden

What are categorised expenses?

Categorised expenses are exactly what they sound like. Instead of submitting a single overall expense figure, businesses provide totals for HMRC’s defined expense categories. These categories include areas such as:

- travel costs

- wages and staff costs

- rent, rates and utilities

- property repairs and maintenance

- advertising and marketing

- professional fees

- phone, stationery and office costs

Under MTD IT, these category year-to-date totals are submitted as part of its quarterly updates. The approach gives HMRC more detailed visibility of business costs throughout the year.

There’s information about the different types of business and property rental income HMRC permits in this article: Declaring expenses under Making Tax Digital for Income Tax: common questions.

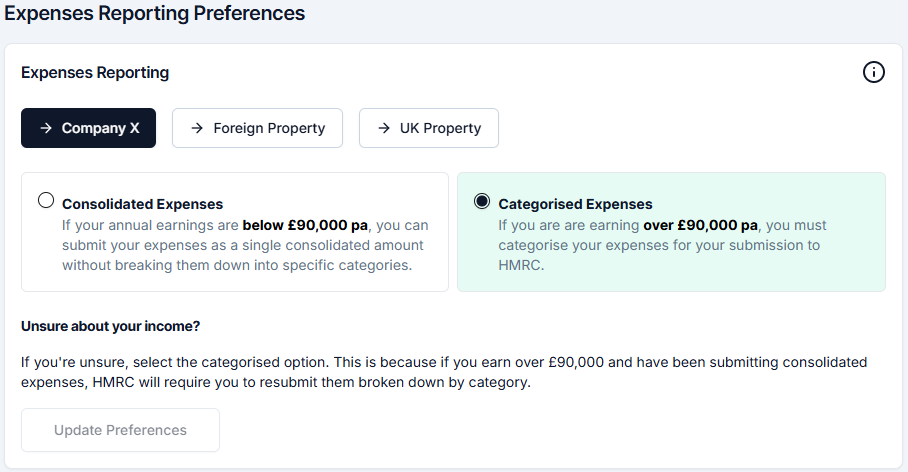

Who can use consolidated expenses?

Under current MTD IT rules, businesses and property income earners with an annual turnover below £90,000 can use consolidated expense reporting.

Once turnover exceeds £90,000 for a particular income source, categorised expenses become mandatory from the start of that tax year.

Importantly, this applies separately to each business or property income source if they have mixed income. For example:

- someone with rental income below £90,000 may still use consolidated expenses for their property business

- while their separate self-employed business above £90,000 may need categorised reporting

This is an important distinction because many people assume MTD IT expense reporting settings apply per taxpayer. In practice, they apply per income source.

That means a person with property income and self-employment operating side-by-side can legitimately use different reporting approaches within the same TaxNav account. They will have to submit a separate quarterly update per income stream, but TaxNav makes the process simple.

What happens if income crosses the threshold?

If business or property income turnover rises above £90,000, individuals will need to move from consolidated to categorised expense reporting in their MTD IT submissions.

The good news is that earlier quarterly updates do not need to be resubmitted to HMRC. However, because categorised expense reporting applies for the full tax year, businesses will still need to review and categorise expenses already recorded earlier in the year before completing later submissions and the annual declaration.

In practice, this means businesses may need to revisit expenses previously included within consolidated totals so they can be allocated into HMRC’s defined expense categories going forward.

How TaxNav helps keep the process simple

One challenge with MTD IT is that different self-employment and property income streams may require different reporting approaches.

Some users want the simplicity of consolidated expenses and spreadsheet-based record keeping. Others may already maintain detailed categorised records throughout the year.

TaxNav is HMRC-recognised MTD IT software designed to support both approaches. Using TaxNav, users can:

- Continue working with spreadsheets if preferred. TaxNav can automatically import the required totals for quarterly updates and the annual declaration to HMRC

- Use our easy-to-use browser-based platform to directly enter information for businesses with simpler records

- Submit MTD IT updates to HMRC quickly and easily through TaxNav’s user-friendly dashboard

- Manage multiple income sources, such as self-employment and property income, within one TaxNav account

- Handle different reporting settings for different business activities, for example using consolidated expenses for one income source and categorised expenses for another, while keeping MTD IT submissions simple and organised

TaxNav is designed to keep MTD IT simple for self-employed people and those with property rental income, whether they prefer spreadsheets or straightforward browser-based record keeping. Its flexibility is also useful for accountants supporting a mixed client base where reporting needs may vary between businesses and property income sources.

Every account comes with an automatic 30-day free trial, and the pricing options are £60+VAT annually or £6+VAT on a monthly pay-as-you-go basis.

Summary

Many businesses are surprised to discover that MTD IT does not always require highly detailed quarterly expense reporting. For smaller businesses and those with property income, consolidated expenses can provide a much simpler route to compliance while still meeting HMRC’s digital requirements.

The key is understanding which approach applies to each income source and using software that handles those differences swiftly and easily. For further reading, see: Declaring expenses under Making Tax Digital for Income Tax: common questions.

See how simple MTD IT can be

Try TaxNav today and discover a simpler way to manage your MTD IT quarterly updates and annual declaration.

Don’t forget, every account includes an automatic 30-day free trial, with pricing at £60+VAT annually or £6+VAT on a monthly pay-as-you-go basis.

Try TaxNav